Beware! Are you in compliance with your cash payments?

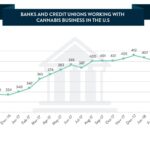

Banks and Credit Unions Working with Cannabis Business in the U.S.

July 15, 2018

Oregon Retail Flower Sales Soar as the Price Per Gram Falls

July 22, 2018

By Mary Amato, CPA, Partner, CohnReznick

It is no secret that the Internal Revenue Service (IRS) is aggressively auditing cannabis businesses. The focus is on more than the limitations placed on the industry by IRC §280E. The IRS aggressively audits non-compliance of Reporting of Cash Payments. Form 8300, is not an income tax reporting form. It is a compliance form required to be filed by any trade or business receiving over $10,000 in cash. Penalties for non-compliance can be steep. Here is insight on what you need to know to avoid these costly penalty fees:

Who Must File

Generally, any person in a trade or business who receives more than $10,000 in cash in a single transaction or in related transactions.

When to File

File by the 15th day after the date the cash transaction occurred. If the 15thday falls on a Saturday, Sunday or holiday the business must file the form on the next business day.

Where to File

The form may be filed electronically using the Bank Secrecy Act (BSA) Electronic Filing (E-filing) System or by mailing the form to the IRS at:

Detroit Computing Center

P.O. Box 32621, Detroit

Michigan 48232

In addition to Form 8300, customers must be provided with an annual statement. The statement must be provided to the customer by January 31 of the following year and should include the following:

- The name and address of the cash recipient’s business

- Name and telephone number of a contact person for the business

- The total amount of reportable cash received in a 12-month period, and

- A statement that the cash recipient is reporting the information to the IRS.

Potential Penalties

Failure to file this form on time results in a penalty of $100 per occurrence. If your business grosses less than $5 million, the penalty is capped at $500,000 per year. However, if the business grosses $1 over $5,000,000, the cap on the penalty is raised to $1,500,000. If you correct the failure to file within 30 days, the aggregate annual penalty limit drops to $75,000. A minimum penalty of $25,000, or the actual amount of the transaction, up to $100,000 (whichever is greater), for each occurrence may be imposed if the failure is due to an intentional or willful disregard of the cash reporting requirements. In addition, there is no annual limit on the penalty for intentionally failing to file Form 8300.

This filing is the responsibility of the business owner and is generally an internal function of the business. Filing of Form 8300 is not a part of the annual income tax returns filed. If businesses have engaged outside professionals, they should specifically understand what is in the scope of the services to be provided.

The IRS Form 8300 Reference Guide should be reviewed to confirm full understanding of reporting obligations. Understanding the who, when and where of the filing responsibilities will help cannabis businesses navigate through the current requirements the IRS has put in place.

This has been prepared for information purposes and general guidance only and does not constitute legal or professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is made as to the accuracy or completeness of the information contained in this publication, and CohnReznick LLP, its members, employees and agents accept no liability, and disclaim all responsibility, for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

For more information on Cannabis Tax, please click here.

{kind=link}

{kind=link}

{kind=link}