For Cannabis Consumers, Inflation is No Obstacle

July 12, 2022

Cannabis Consumers’ Decreased Spending Is Balanced by Enthusiasm

July 26, 2022For Cannabis Consumers, Inflation is No Obstacle

July 12, 2022Cannabis Consumers’ Decreased Spending Is Balanced by Enthusiasm

July 26, 2022

by Noah Tomares, Senior Research Analyst, New Frontier Data

Analysis of the cannabis industry is often considered through a macro lens because data is generally gathered at the statewide or national level. While it is worthwhile to note that overall legal sales of cannabis in the United States (i.e., in both medical and adult-use markets) are projected to grow from $32 billion this year to over $72 billion in 2030, such assertions do little to explain how a specific state or municipality’s market might deviate from broader trends. It is imperative for producers and brands to understand both the macro and micro characteristics that shape the particular conditions of each market where they aspire to succeed.

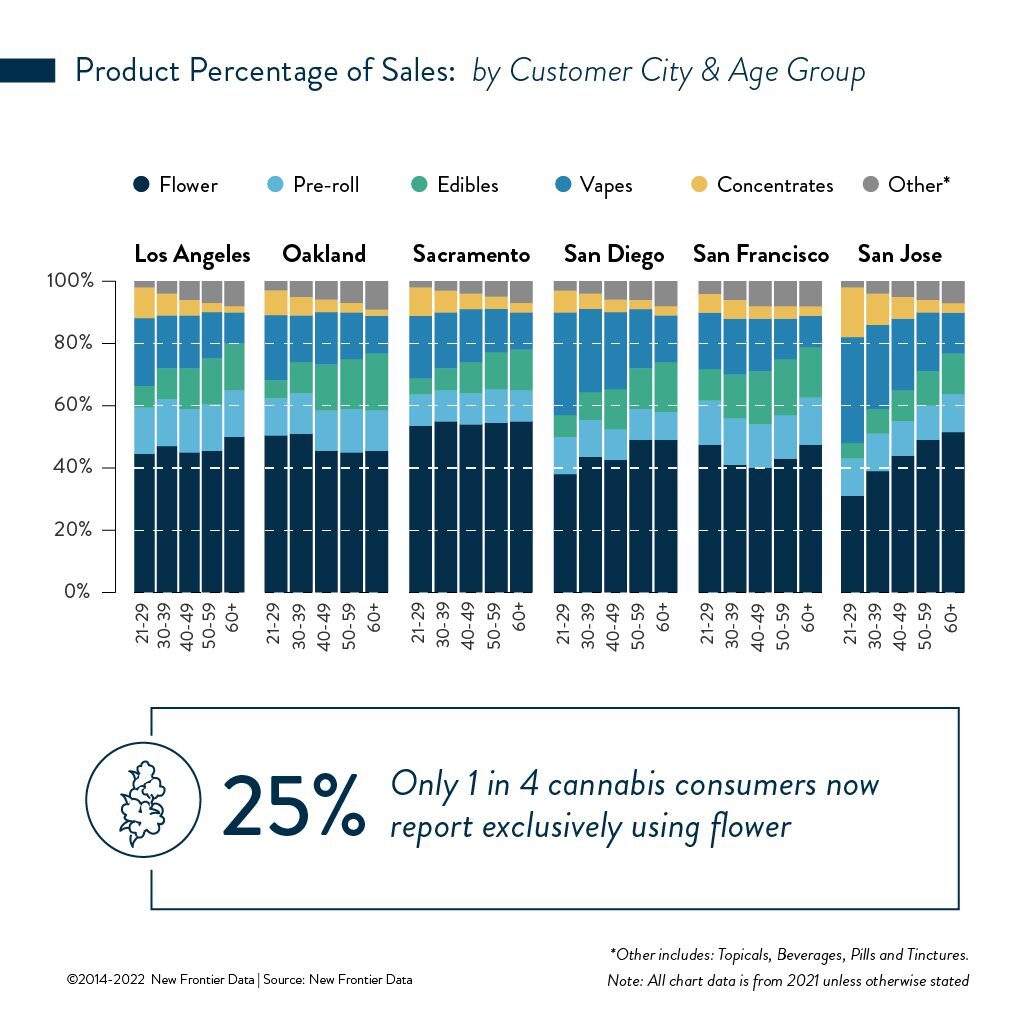

From a macro perspective, most (57%) consumers now choose both flower and non-flower products. One 1 among 4 (25%) report exclusively using flower, while 17% prefer only non-flower forms. For consumers who use multiple forms of cannabis, their choice of activity is the leading determinant (46%) for the form used. At the micro level, variability in market conditions and consumer populations can substantially affect a product’s relative market share.

A quick look at Equio’s Consumer Data dashboard indicates that 74% of Californian consumers use smokeables. But, among six major California cities (e.g., Los Angeles, Oakland, Sacramento, San Diego, San Francisco, and San Jose), there is substantial variation among legal product purchases. Flower and pre-rolls had the largest combined share of sales in Sacramento, accounting for nearly two-thirds (64%) of the cannabis consumed there. Notably, pre-rolls made up a smaller proportion (10%) of sales) than among any of the other metro populations sampled and described in New Frontier Data’s latest report, The Power of Flower.

Consumers in San Diego and San Jose, respectively, bought less flower than in other cities, though flower and pre-rolls in those locales accounted for more than half (54% and 51%, apiece) of all legal sales.

Similarly, observing purchasing behaviors by gender also reveals distinct product preferences. In each analysis, men purchased more loose flower, while women purchased more pre-rolls. A consumer’s age demonstrated a more significant influence on preferred product types. Cartridges and extracts were most popular among consumers in the youngest cohort, regardless of city of origin. For consumers in San Jose and San Diego, older individuals were much likelier to purchase flower, while younger cohorts chose cartridges. Noting the youngest subset of consumers from San Jose, extracts and cartridges comprised half (50%) of purchases, while among their neighbors aged 60 or older cartridges and extracts accounted for less than 1/6 of sales.

In cities lacking such outsized shares in younger cohorts’ purchases, flower sales per age brackets were far more consistent. In Sacramento, where consumers report purchasing flower at the highest rates sampled, flower dominated preferences across all age groups. Similarly, pre-roll sales seemed consistent across age groups relative to their city. Edible purchases tended to gain popularity in relation to customers’ ages. Even so, they did not appear to cannibalize flower sales in the way that cartridges do for younger consumers.

The increasing availability of value-added products affords consumers more options for integrating cannabis into their lifestyles. Choices for product types are fragmenting as consumers become more disparately intentional with their use — i.e., selecting different products (and related effects) for different purposes. Flower currently dominates sales at a macro level, but the consumers exclusively consuming flower represent a shrinking minority. It will be imperative for flower brands to understand how the hastening fragmentation of use will impact demand for their products.

{kind=link}

{kind=link}

{kind=link}